Keep in mind that refinancing isn’t free. Just like your original mortgage, you’ll have to pay closing costs—typically 3% to 6% of your new loan principal, according to Freddie Mac. If consolidating your debts doesn’t save you at least this much, refinancing might not be worth it in the long run.

Before making a decision, calculate your breakeven point—the moment your refinance starts saving you more than it costs. If you don’t plan on staying in your home beyond that point, refinancing may not be a wise choice.

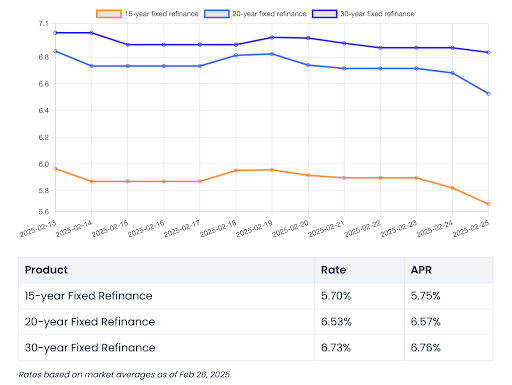

Use our refinance breakeven calculator to see if this strategy makes sense for you.

A cash-out refinance is a good option if it reduces your total interest payments and covers the closing costs.

"If you have a significant amount of high-interest debt and aren’t making real progress with monthly payments, a cash-out refinance could be a smart move," says Debra Shultz, Vice President of Lending at CrossCountry Mortgage. "Mortgage rates are generally lower than credit card and personal loan rates."

Shultz advises speaking with a mortgage professional to crunch the numbers and determine if this strategy aligns with your financial goals.

"The biggest savings I’ve seen was a few years ago," Shultz recalls. "I helped a client refinance and cash out to pay off $200,000 in credit card debt. Not only did I lower their mortgage rate, but I also reduced their total monthly payments by $6,000. They were beyond thrilled."

Let’s say your current mortgage rate is 8%, and you have two credit cards with 20% interest rates. If you qualify for a 7% cash-out refinance, you could save a significant amount in interest over time—assuming you plan to stay in the home long enough to offset closing costs.

If your current mortgage rate is 5% but refinancing would give you a 7% rate, using a cash-out refinance might not be the best move.

While you’d lower the interest on your debts, you’d also increase the interest on your mortgage, which is typically a much larger loan. In this case, the long-term costs may outweigh the benefits.

A cash-out refinance isn’t the only way to consolidate debt. Consider these alternatives:

Home Equity Loan or HELOC – Tap into your home’s equity without replacing your current mortgage.

Reverse Mortgage – If you’re a senior, this could provide another option.

Balance Transfer Credit Card – Some offer 0% interest for a year or more, giving you time to pay off debts without accruing additional interest (though balance transfer fees apply).

Debt Consolidation Loan or Personal Loan – These can be helpful, but rates vary widely based on credit score.

Consolidating debt can make payments more manageable, but it won’t solve the underlying issue if overspending is a recurring problem.

"It’s a bad idea if you’re not disciplined and likely to run up credit card balances again," Shultz warns.

If you struggle with spending habits, consider working with a credit counselor or financial planner to create a sustainable financial plan.

At FedCutRates.net, we believe that knowledge is power—especially when it comes to making important financial decisions.