There are no restrictions on how you use the funds from an FHA cash-out refinance. Homeowners commonly cash out equity for:

Home improvements and renovations

Consolidating high-interest debt

Paying off HELOCs and second mortgages

Purchasing a second home or investment property

Covering major expenses like college tuition or a wedding

FHA cash-out refinances have more flexible qualification criteria than many other mortgage options. Here’s what you need to know:

A minimum credit score of 580 is typically required.

FHA guidelines allow scores as low as 500, but most lenders set their own higher limits.

Cash-out refinances are considered riskier, so expect stricter lender requirements.

The maximum LTV for FHA cash-out refinances is 80%.

This means your new loan cannot exceed 80% of your home’s appraised value after cashing out equity.

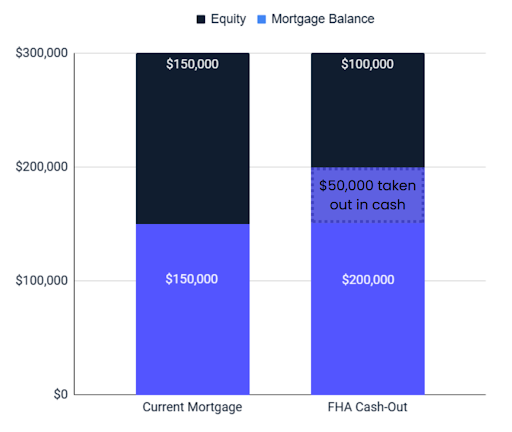

Example:

If your home is worth $250,000, the maximum LTV allows a loan of $200,000.

If you owe $150,000 on your current mortgage, you could cash out $50,000 (minus closing costs).

FHA lenders generally allow a DTI between 43% and 50%.

Borrowers with strong compensating factors may qualify with a DTI as high as 56.9%.

Example:

If you earn $6,000 per month, have a $1,500 mortgage, and a $500 car payment, your DTI would be just over 33% ($2,000 / $6,000).

FHA cash-out refinances are only available for primary residences.

You must have lived in the home for at least 12 months before applying.

You must certify that you will continue living in the home for at least one more year after refinancing.

You must have on-time mortgage payments for the last 12 months.

This includes payments for any second mortgage on the property.

FHA loans require both upfront and annual mortgage insurance premiums (MIP):

1.75% upfront MIP (added to your loan amount)

0.5% annual MIP for most borrowers

If you took out your original FHA loan less than three years ago, you may qualify for a partial UFMIP refund.

In 2025, the FHA loan limit for most areas is $524,225 for a single-family home.

High-cost areas have increased limits up to $1,209,750.

The highest limits apply in Alaska, Hawaii, Guam, and the U.S. Virgin Islands, where a single-family home can qualify for up to $1,814,625.

Use HUD’s FHA Mortgage Limits Tool to check loan limits in your area.

FHA loans are backed by the government, which reduces lender risk and often results in lower interest rates compared to conventional loans—especially for borrowers with lower credit scores.

Let’s take a look at how FHA refinance rates are trending compared to conventional refinance rates:

At FedCutRates.net, we believe that knowledge is power—especially when it comes to making important financial decisions.